My firstborn (FB for identification purposes in the rest of this post) is 22 years old. I thought I would have taught them everything I could by now, life skills wise. It started with things like tooth brushing and pouring drinks. I turned over laundry duties nine years ago. A driver’s license has been in hand for five years. The kid has held a responsible, paying job for fifteen months, and even managed tax filing without my help this year.

But life is always throwing something new at you. I currently find myself in the midst of assisting Kid A with the messy art of disputing medical billing. Perhaps you’ve read some articles recently about surprise emergency room charges. We’re living it.

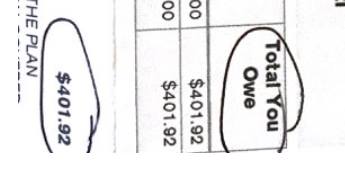

It all stems from a late-night sudden illness last June. The insurance benefits posted on-line made it look like a trip to the ER should cost a total $100 copay. I offered to split the cost of the bill. Going to the ER turned out to be the right medical decision, but a second trip was nearly induced a couple of months later for heart issues when the health insurance statement showed up, claiming the total patient responsibility was $401.92. Whoa Nelly!

FB tried calling to straighten it out, but quickly became overwhelmed by the bureaucrat-speak, and gave permission for me to handle the issue. I made sure they knew every at step what I was doing, because dealing with health insurance snafus is sure to be a recurring issue in every American life.

I wish I could say I resolved the problem, but it’s still ongoing. In fact, I have a formal complaint filed with our state’s insurance commission and have also contacted the attorney general’s office to see if they can offer advice.

I did teach my kid some specifics for handling communications, though. Document all phone calls, taking names and writing down what was said. When the recorded voice tells you this call may be recorded for quality assurance purposes, keep that in mind. Don’t inadvertently go on record sounding like you agree with anything you really know is wrong. For a Midwesterner raised to be agreeable and pleasant at all times, this is hard. I keep wanting to say, “Okay. I see.” Instead I say, “No, that’s not right.”

Of course, the insurance company gave me the run-around, saying they would send the claim back for review, followed by radio silence until I initiated contact again. Then all of their stories changed when I talked to a second, different person. The real kicker is that, in the meantime, the hospital bill arrived and it was $501.92, even a hundred more than the surprise amount on the insurance statement.

I thought at least that extra hundred would be easy to straighten out. Simply show the hospital billing office the EOB we received. Nope. In November, I called and agreed to pay the $401.92 (FB kicking in the original $50 they agreed to), with the understanding we were still working on the insurance company to get things fixed and we would expect a $300 refund eventually. I worry about bad credit. I was told yes, to pay that amount and fax them a copy of the EOB I had. I did as told and assumed we were finished dealing with them until we could harass the insurance company into doing the right thing.

Nope. A couple of weeks ago, FB got a rude young adult awakening with a letter out of the blue from a collection agency, stating they owe an unpaid bill of $100 to the hospital. I got on the phone with the hospital again, with FB listening, and was able to read them my notes from all previous phone calls to them and insurance company. I said I would once again send them copies of the insurance statement we received, which clearly said “Total patient responsibility: $401.92.” I got an email address this time and scanned the letter to them.

The next day, FB and I were both off work, so we drove to the hospital billing office and presented the paperwork in person, proof it hadn’t been altered in any way. The woman who helped us was as confused as I. She said, “That’s sure what they told you, but when I look it up online, it tells me $501.92.” I talked her into calling the collection agency and putting a hold on their collection efforts until we got the bill straightened out.

After providing proof three different ways, we walked away expecting a phone call from the hospital stating their bill had been corrected. Guess what, though? Right – radio silence again. I finally called back a week later and ended up with a manager, who insisted the higher amount was correct because it’s what they see on the computer. The only way they could change their bill was to get a new, revised EOB from the insurance company.

But when I called them, the representative refused to issue one, saying, “I’m looking here and it says $501.92.” I also emailed them scans of the statement they sent me. Back on the phone with the billing manager, she said she talked to someone at insurance who told her basically that I was lying, that I had simply withheld pages of our insurance statement from her, and if I looked on the very last page, there it said we “might” owe $501.92. I apprised my kid of the latest developments and showed them how to dig in. I went back to the hospital in person again on my day off and presented in person the entire insurance statement I had received, which had the number $501.92 nowhere on it. In fact, the last page was only a list of how to get information if you speak a language other than English.

After hours worth of phone calls, with ever shifting stories from our health insurance company, my temporary, wimpy resolution of the issue was to drive a third time to the hospital billing office, agreeing to pay the $100 only to get the account out of collections and save my child’s credit rating here at the beginning of their adult life. But I also filed a formal complaint in writing to the insurance company and to the insurance commission, and insisted on a note being put on the account stating we didn’t agree the amount was owed.

My biggest concern was that, if they’d already moved the goalposts twice, they could move them again. I was afraid we’d hand them another $100 and then in three months, they might decide the total owed was actually $600, or $800 and ding us again. So I paid the hundred only under the condition that they cancel the collection agency altogether while I was sitting there to witness it and they print me a statement showing a zero balance on the account.

Now, we are waiting to hear back from the insurance commission or attorney general’s office. The thing is, if they had only been a large amount greedy, I would have let it go at 400. But when they went from large greedy to huge greedy and threw in some gaslighting on top of it, they transformed the whole issue into the hill on which I was willing to die. Now I’m working to get a full refund.

I know it’s most likely we’ll get nothing, but I hope at least I’m showing my kid that you keep standing up for yourself. If a bureaucrat is going to swindle you, you should at least make them work for it.

Wow. Talk about persistence! I’m almost certain I wouldn’t have kept at it like that. I learned a couple tips from your post.

Keep up your amazing work!!!

Thanks. It doesn’t feel too amazing as we get the runaround and still haven’t reached a resolution. But at least we’re not going down without a fight.